Today’s post is from Eric Strovink, the spend slayer of spendata. real savings. real simple. Eric was previously CEO of BIQ; before that, he led the implementation of Zeborg’s ExpenseMap, which was acquired by Emptoris and became its spend analysis solution.

When you join transaction data to contract data in order to validate contract price compliance, it is possible to discover lots of interesting information. Some if it can be quite surprising.

For example, you might notice that off-contract items make up a surprisingly large proportion of the spending. This may be trending up with time, so it is worth doing a time-series analysis. You might also notice a pattern of overcharges on particular items, which could be an easily-corrected disconnect at the vendor side on contract terms.

In Excel, these analyses require new pivot tables and, concomitantly, more maintenance effort on refresh. But in a spend analysis system, the model can be augmented with additional pivot-table-equivalents in seconds, with just a few mouse clicks. And, refresh is not an issue, because the spend analysis system updates everything automatically upon loading new transactions. So, much more interesting analyses become real possibilities — including monitoring demand.

The Who

Suppose that we have from the vendor not only the item pricing, but also an idea of who within the organization is doing the purchasing. This then enables us not only to identify off-contract spending, but also find the source of the leakage within the organization, so that corrective action can be taken internally.

There are a number of ways that “Who bought the items” can find its way into PxQ data. Sometimes it is present as a matter of course; sometimes it requires effort.

- If the item is a catalog buy or punch-out, invoice items likely already contain the cost center.

- If a PO number was provided to the vendor, invoice items should contain the PO. The PO can be easily translated to cost center (well, “easily” if the PO data can be linked in, as it can be with a spend analysis system).

- If there’s a useful delivery address on the invoice, that can be mapped to a cost center using the spend analysis system’s mapping tools (of course, you need access to the mapping tools, and they need to be simple to use).

- Your contract with the vendor could require a cost center to be provided on the invoice as a prerequisite for payment. No cost center, no payment.

- Corporate purchasing cards are by definition associated with a cost center, so these can be mapped to cost center using the spend analysis system’s mapping tools.

- Consultants put project codes on invoices; lawyers put matter numbers. These can be mapped to cost centers as well. Any invoice without a project code or matter number shouldn’t be paid.

- Some spend already has a fixed cost center, for example with copiers. Each copier is assigned a cost center, which shows up on the invoice.

In a nutshell, if you want to have a cost center attached to each row of an invoice, it is very doable, and very worthwhile.

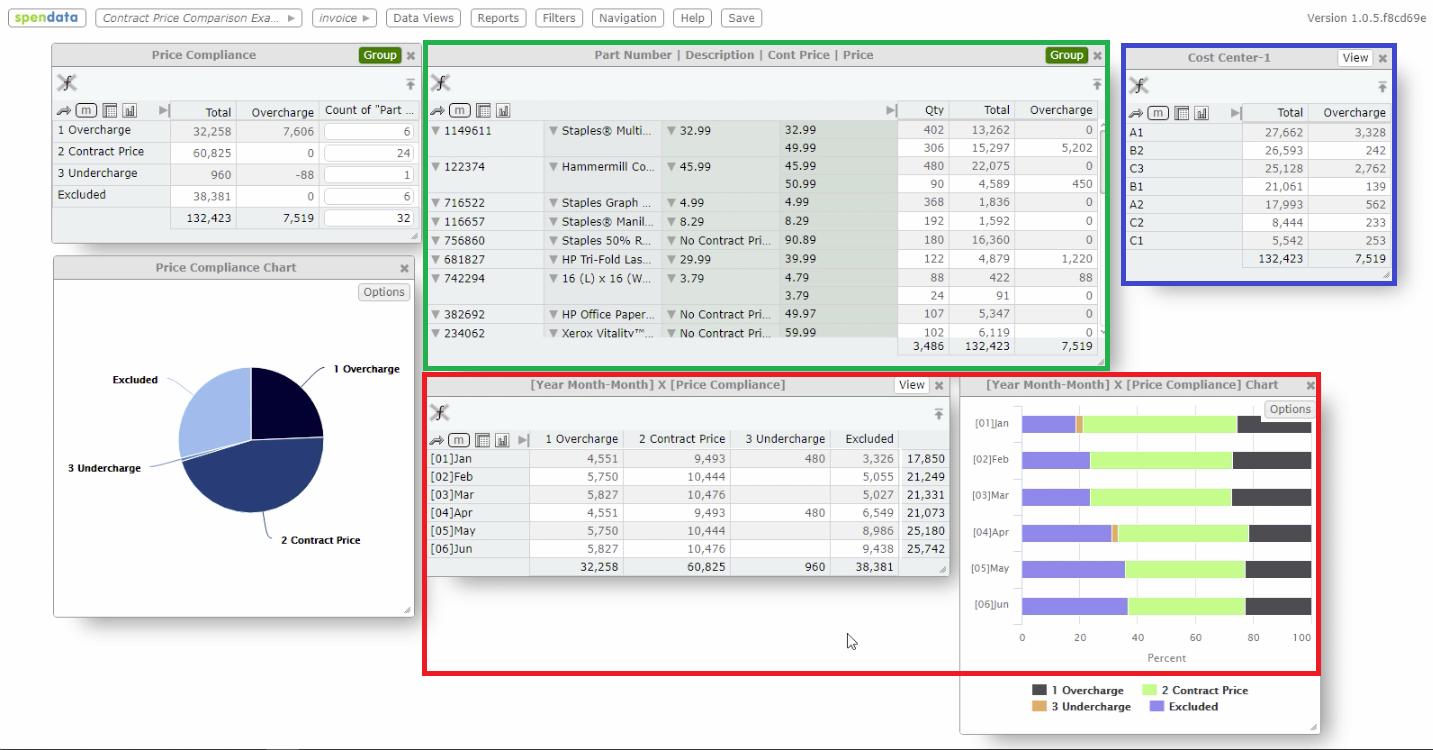

Let’s revisit the dashboard from Part II.

- We can see a breakdown of overcharge buys by cost center (blue). A similar breakdown of off-contract items helps identify who is buying off-contract. There may be very good reasons for this, of course; and those reasons need to be understood, so that we can either get those items onto the contract, or channel the buying to similar items that are on contract.

- We can see a time-series analysis of item buys by class, with an associated chart (red). Over time, fewer items are being bought with the contract price, which is not a good trend.

- We can see all the buys, showing both contract and overcharged prices (green). This is all we need to show to the vendor — just dump it to Excel, email the spreadsheet, done.

The basic pattern of this type of analysis doesn’t change with the commodity. Providing that the goods or services can be standardized with a fixed price, and that a contract price is available, the technique is always the same — and the analysis always worthwhile, if only to prove that the contract is in place and actually working.

Thanks, Eric!