Or at least the deal?

Last year Icertis raised over 100 Million at a valuation that allowed it to become the next unicorn and Coupa bought Exari to fill the hole in their suite. Seal Software raised another 15 Million just to power contract discovery and a new startup, Lexion, raised 4.2M to bring AI to contract management.

Pure-play CLM, and its precursor technology, has been around for a long time. Exari was founded in 1999 and Selectica, which rebranded as Determine after it acquired b-pack and Iasta, dates back to 1996 when it offered a CPQ (configured price quote) solution. Not long after, Nextance (which was acquired by Versata) was founded in 2000. And the saga continued from there.

But we won’t bore you with a detailed recounting of providers that have come and gone over the past 20 years. The point was merely to make it clear that while CLM has been around for a long time, it hasn’t been very successful. The majority of providers have been acquired, acquired, and/or morphed into different solution providers in order to survive.

But this is the year CLM may finally come to the forefront. With risks increasing, costs escalating, and supply chains lengthening, contracts, and associated obligation and liability management, are becoming ever more important. It’s not just negotiating a good deal, it’s ensuring that deal is adhered to. That’s more than just loading the items into the catalogue with agreed to pricing and ensuring the invoices match the purchase orders, it’s ensuring the items are bought when they are supposed to be (so the company keeps its end), delivered when they are supposed to be, at the quality level they are supposed to be at, and free of the risks they are supposed to be free of.

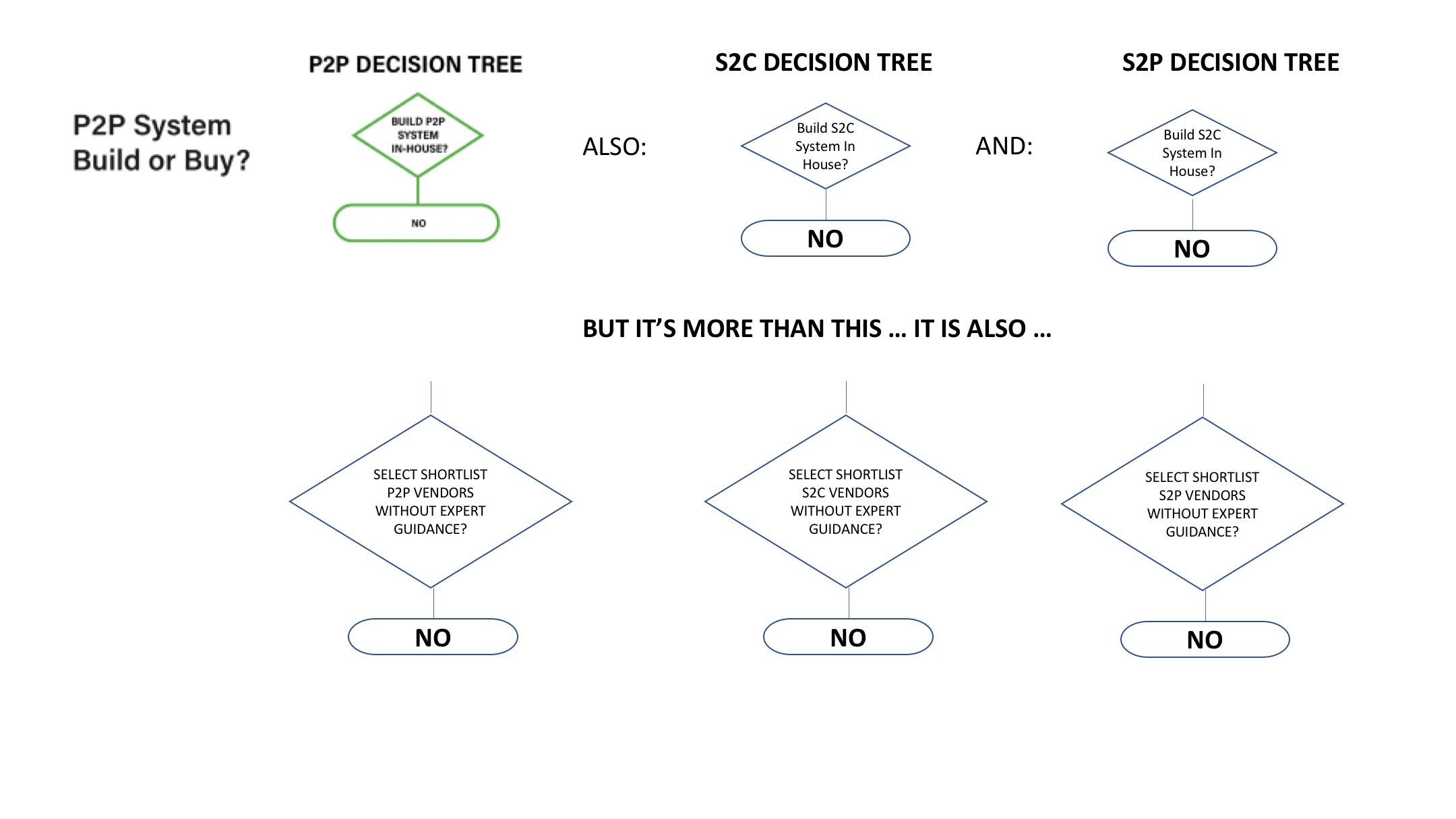

This requires not only careful monitoring of execution, but careful construction and review (are there any clauses with ambiguous interpretations or would counter-party suggestions increase risk), and this is a capability most Source-to-Pay providers don’t have. When most vendors advertise contract management, what they really have are contract meta-data management — the system can track contracts, products and services, pricing, promised demands, and associated contract documents, but can’t suggest templates, analyze them, or intelligently determine when an obligation isn’t being met by either party. The systems can’t intelligently manage clause libraries or help with intelligent contract drafting, comparison, or exception management.

But if contracts are the only cure to the ills of risk and obligation management, considering the difficulty most organizations have in finding and getting a handle on them, then this might be the year that CLM finally comes into its own. It may not break the bank, but it may start being the differentiator in deals. And that may just be enough.