Today’s post is from Eric Strovink, the spend slayer of spendata. real savings. real simple. Eric was previously CEO of BIQ; before that, he led the implementation of Zeborg’s ExpenseMap, which was acquired by Emptoris and became its spend analysis solution.

If you have a contract with a vendor, that’s good news — you’re not paying list prices any more. At least, that’s what should be happening.

It’s fascinating what can really happen. We’ve recently seen a vendor raise prices in a distant region while maintaining contract prices in the headquarters region. This and similar disparities aren’t necessarily deliberate — mistakes can be made by anyone. Even items purchased through an e-procurement system can fall off the price-compliance applecart as a result of exception-handling processes. The lesson is that “Trust but Verify” is a necessity, not a nicety. And, since manual inspection of a large volume of items and invoices is impossible, this process must be mechanized.

The good news is that many goods and services can be standardized with a fixed price. These items can easily constitute 25-30% of spending. For these goods and services, contract compliance is (at least conceptually) straightforward. Examples include physical items, such as computers, office supplies, phones, furniture, MRO parts, facilities supplies, vending items, security equipment, mobile phone plans, stationery and forms, promotional items — even some types of software. Services examples can include cleaning, appraisals, training classes, recruiting, records management, armored car, overnight mail, hotel, and car rentals (when they are for a fixed unit of time or work).

If contract compliance for these goods and services is straightforward, why doesn’t everyone do it? As usual, the devil is in the details.

- Who builds the (usually spreadsheet) compliance model?

- Does the model show who is buying off-contract items from the vendor? Which items? When?

- Who loads next month’s data into the model, and adapts it accordingly? What’s the cost of this, versus the payback?

For these questions, invoice data, aka Price X Quantity (PxQ) data, is required.¹

Acquiring Data

PxQ data is best acquired directly from the vendor. It’s your data; you have a right to it; and you’ve a right to ask for it. Many vendors will supply it in a reasonable format, such as in an Excel spreadsheet, or as a CSV or DSV file. Some vendors, though, will attempt to discourage you by providing data in an unreasonable format — for example, by supplying every invoice they’ve sent, in PDF format, as an individual file (don’t laugh; we’ve seen this). You may want to consider whether doing business with that vendor is in your best interest moving forward. Certainly you should write into any future contract that the vendor must provide PxQ data in a reasonable format.

But, you also need contract data — that is, contract price by item. That data is probably already in a reasonable format, for example as an addendum to the contract. At worst, it can be keyed in manually or minimally edited into shape.

So, there are two datasets to consider. The first, consisting of invoice level PxQ data, comes from the vendor and resembles this:

![]()

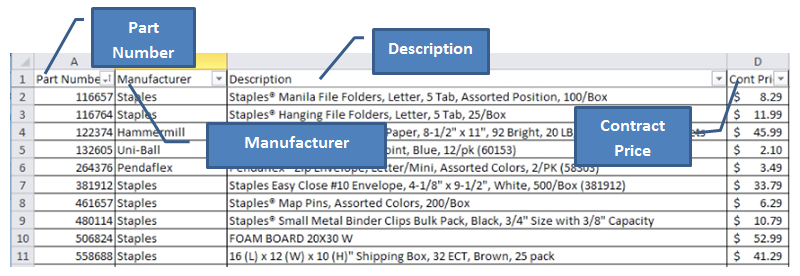

The contract pricing, which you should already have, resembles this:

Once you have the data in this form, you can easily figure out whether the contract is leaky or solid. We’ll continue this discussion in Part II, Monitoring the vendor.

Thanks, Eric!

¹Accounts Payable-based spend analysis can help to determine what spend is definitely not under contract. But it is helpless to address contract compliance issues.